Carlos, director of a gardening company with 15 employees, knew that his sales fluctuated according to the seasons, but he had never quantified exactly when and how much. Every spring he ran out of stock of key products, while every winter he accumulated inventory that didn't move until months later. His accountant suggested hiring more staff in summer, but he wasn't sure exactly when or for how long.

Carlos's story is that of thousands of SMEs that operate 'blindly' regarding the temporal patterns of their business. Time series analysis converts those hidden patterns into actionable information, enabling strategic planning based on real data instead of intuition.

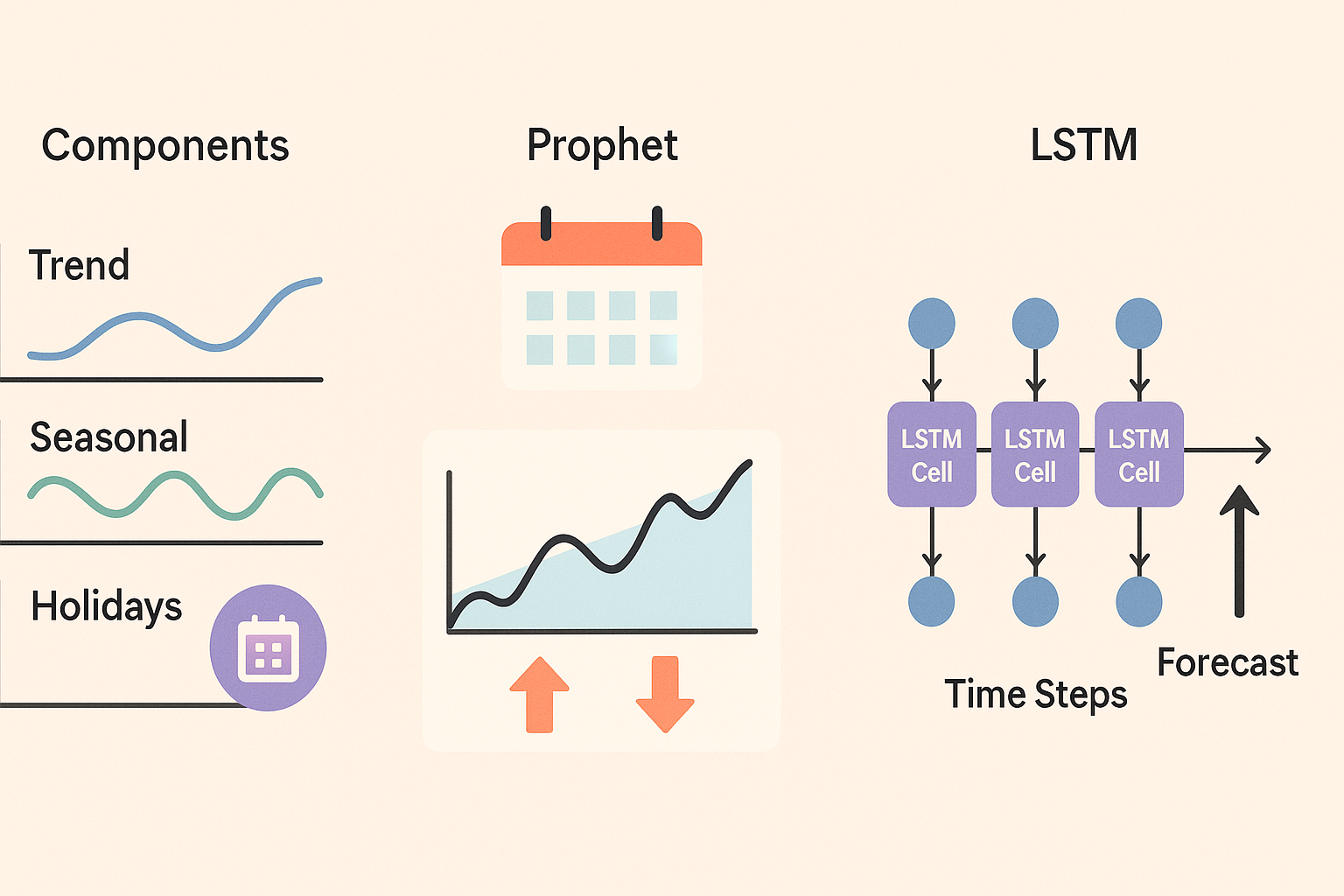

What is Time Series Analysis?

A time series is simply a sequence of chronologically ordered data: monthly sales, daily number of customers, quarterly revenue, weekly website visits. Time series analysis studies this data to identify patterns, trends, and cycles that allow predicting future values.

For an SME, this means transforming historical data it already possesses into strategic information for making planning, hiring, purchasing, marketing, and operations decisions. It's like having a time machine that reveals what to expect in the coming months based on what has already happened.

The Four Fundamental Components

Every business time series can be decomposed into four basic elements that, once identified, allow complete understanding of business behavior and making accurate predictions.

1. Trend: The General Direction

The trend shows whether your business is growing, stagnant, or declining in the long term. It's the underlying pattern when we remove daily, weekly, or seasonal fluctuations.

- Growing trend: Sales increase consistently month after month

- Declining trend: Gradual decline in product demand

- Stable trend: Mature business with horizontal growth

- Cyclical trend: Growth and decline in long periods (2-10 years)

2. Seasonality: Predictable Patterns

Demand seasonality are regular and predictable fluctuations that repeat in specific periods: daily, weekly, monthly, or annual.

| Business Type | Seasonal Pattern | Practical Example |

|---|---|---|

| Fashion retail | Annual | Peaks in spring/autumn, decline in January |

| Restaurant | Weekly | Maximum Friday-Sunday, minimum Monday-Tuesday |

| E-commerce | Daily | Peaks 8:00-10:00 PM, minimum 4:00-6:00 AM |

| Tourism | Annual | Maximum summer, minimum winter |

| B2B services | Monthly | Decline in August and December |

| Financial products | Quarterly | Peaks at the end of each quarter |

3. Cycles: Irregular Fluctuations

Cycles are fluctuations that don't have a fixed periodicity like seasonality. They are influenced by economic factors, industry changes, or external events.

- Economic cycles: Recessions, expansions, financial crises

- Technological cycles: Adoption of new technologies, obsolescence

- Competitive cycles: Entry of new competitors, price wars

- Regulatory cycles: Changes in laws, regulations, taxes

4. Noise: Random Variations

Noise are random fluctuations that don't follow any identifiable pattern. They represent unique events, measurement errors, or unpredictable factors.

The goal of time series analysis is to separate these components to understand what is predictable (trend, seasonality) and what is random (noise), allowing for more accurate projections.

Practical Use Cases for SMEs

Business trend analysis has immediate applications in multiple areas of any SME. Each department can benefit from more accurate predictions to optimize resources and planning.

Sales and Marketing Planning

- Monthly/quarterly revenue prediction for budgets

- Identification of high demand periods to intensify marketing

- Promotional campaign planning based on historical seasonality

- Advertising budget allocation according to conversion patterns

- Early detection of declines in specific products

Human Resources Management

- Temporary staff hiring for seasonal peaks

- Team vacation planning during low demand periods

- Work schedule adjustment according to activity patterns

- Variable payroll budget based on sales projections

- Identification of training needs according to business cycles

Financial Optimization

- Monthly cash flow prediction for liquidity management

- Investment planning during periods of higher profitability

- Credit line negotiation based on seasonal patterns

- Supplier payment optimization according to income cycles

- Financial reserves calculated according to historical variability

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from statsmodels.tsa.seasonal import seasonal_decompose

from statsmodels.tsa.holtwinters import ExponentialSmoothing

from datetime import datetime, timedelta

class TimeSeriesAnalyzer:

def __init__(self, data):

"""

Initializes the analyzer with time series data

data: DataFrame with 'date' and 'value' columns

"""

self.data = data.copy()

self.data['date'] = pd.to_datetime(self.data['date'])

self.data = self.data.set_index('date').sort_index()

self.components = None

self.model = None

def decompose_series(self, seasonal_period=12):

"""

Decomposes the series into trend, seasonality, and noise

"""

self.components = seasonal_decompose(

self.data['value'],

model='multiplicative',

period=seasonal_period

)

return self.components

def visualize_components(self):

"""

Creates graphs of the series components

"""

if self.components is None:

self.decompose_series()

fig, axes = plt.subplots(4, 1, figsize=(15, 12))

# Original series

self.components.observed.plot(ax=axes[0], title='Original Series')

axes[0].set_ylabel('Value')

# Trend

self.components.trend.plot(ax=axes[1], title='Trend', color='orange')

axes[1].set_ylabel('Trend')

# Seasonality

self.components.seasonal.plot(ax=axes[2], title='Seasonality', color='green')

axes[2].set_ylabel('Seasonal Factor')

# Noise

self.components.resid.plot(ax=axes[3], title='Noise/Residuals', color='red')

axes[3].set_ylabel('Residuals')

plt.tight_layout()

return fig

def calculate_seasonal_statistics(self):

"""

Calculates useful statistics about seasonality

"""

if self.components is None:

self.decompose_series()

# Extract seasonal component

seasonal = self.components.seasonal.dropna()

# Calculate statistics by period

statistics = {

'maximum_factor': seasonal.max(),

'minimum_factor': seasonal.min(),

'seasonal_variation': seasonal.max() - seasonal.min(),

'peak_period': seasonal.idxmax().month if hasattr(seasonal.idxmax(), 'month') else seasonal.idxmax(),

'valley_period': seasonal.idxmin().month if hasattr(seasonal.idxmin(), 'month') else seasonal.idxmin(),

'coefficient_variation': seasonal.std() / seasonal.mean()

}

return statistics

def train_prediction_model(self, prediction_horizon=12):

"""

Trains Holt-Winters model for prediction

"""

# Determine if there's significant seasonality

if self.components is None:

self.decompose_series()

statistics = self.calculate_seasonal_statistics()

has_seasonality = statistics['coefficient_variation'] > 0.1

# Configure model

if has_seasonality:

self.model = ExponentialSmoothing(

self.data['value'],

trend='add',

seasonal='mul',

seasonal_periods=12

).fit()

else:

self.model = ExponentialSmoothing(

self.data['value'],

trend='add'

).fit()

# Make predictions

predictions = self.model.forecast(prediction_horizon)

# Calculate confidence intervals (approximate)

error_std = np.std(self.model.resid)

lower_interval = predictions - 1.96 * error_std

upper_interval = predictions + 1.96 * error_std

return {

'predictions': predictions,

'lower_interval': lower_interval,

'upper_interval': upper_interval,

'model_info': {

'aic': self.model.aic,

'has_seasonality': has_seasonality,

'average_error': error_std

}

}

def generate_insights_report(self):

"""

Generates report with business insights

"""

if self.components is None:

self.decompose_series()

statistics = self.calculate_seasonal_statistics()

# Analyze trend

trend = self.components.trend.dropna()

annual_growth = ((trend.iloc[-12:].mean() / trend.iloc[:12].mean()) - 1) * 100

# Volatility

volatility = self.data['value'].pct_change().std() * 100

report = {

'trend_summary': {

'annual_growth_pct': annual_growth,

'direction': 'Growing' if annual_growth > 5 else 'Declining' if annual_growth < -5 else 'Stable'

},

'seasonality_summary': {

'maximum_variation_pct': (statistics['seasonal_variation'] - 1) * 100,

'peak_month': statistics['peak_period'],

'valley_month': statistics['valley_period'],

'is_significant': statistics['coefficient_variation'] > 0.1

},

'volatility': {

'monthly_volatility_pct': volatility,

'level': 'High' if volatility > 20 else 'Medium' if volatility > 10 else 'Low'

},

'recommendations': self._generate_recommendations(annual_growth, statistics, volatility)

}

return report

def _generate_recommendations(self, growth, statistics, volatility):

"""

Generates specific recommendations based on analysis

"""

recommendations = []

# Trend-based recommendations

if growth > 10:

recommendations.append("Consider expanding operational capacity to sustain growth")

recommendations.append("Plan hiring additional staff")

elif growth < -10:

recommendations.append("Review commercial strategy - significant decline detected")

recommendations.append("Consider product or market diversification")

# Seasonality-based recommendations

if statistics['coefficient_variation'] > 0.2:

recommendations.append("Plan inventory and staff according to seasonal patterns")

recommendations.append("Consider complementary products to stabilize income")

# Volatility-based recommendations

if volatility > 25:

recommendations.append("Maintain financial reserves to manage high volatility")

recommendations.append("Implement alert system for sudden changes")

return recommendations

# Example usage with simulated data

np.random.seed(42)

dates = pd.date_range('2022-01-01', '2024-12-31', freq='M')

# Simulate series with trend, seasonality, and noise

trend = np.linspace(1000, 1500, len(dates))

seasonality = 100 * np.sin(2 * np.pi * np.arange(len(dates)) / 12)

noise = np.random.normal(0, 50, len(dates))

values = trend + seasonality + noise

example_data = pd.DataFrame({

'date': dates,

'value': values

})

# Create analyzer

analyzer = TimeSeriesAnalyzer(example_data)

# Decompose and analyze

components = analyzer.decompose_series()

report = analyzer.generate_insights_report()

predictions = analyzer.train_prediction_model(6)

print("=== TIME SERIES ANALYSIS REPORT ===")

print(f"Annual growth: {report['trend_summary']['annual_growth_pct']:.1f}%")

print(f"Direction: {report['trend_summary']['direction']}")

print(f"Maximum seasonal variation: {report['seasonality_summary']['maximum_variation_pct']:.1f}%")

print(f"Volatility: {report['volatility']['level']} ({report['volatility']['monthly_volatility_pct']:.1f}%)")

print("\nRecommendations:")

for rec in report['recommendations']:

print(f"- {rec}")Data Needed to Get Started

One of the advantages of time series analysis is that it uses data that most SMEs already collect routinely. You don't need to invest in new capture systems: your existing records contain valuable information waiting to be analyzed.

Essential Basic Data

| Data Type | Common Source | Minimum Frequency | Minimum Period |

|---|---|---|---|

| Sales/Revenue | Billing, POS, E-commerce | Daily | 12 months |

| Number of customers | CRM, Database | Weekly | 18 months |

| Inventory/Stock | ERP, Spreadsheets | Weekly | 12 months |

| Web visits/traffic | Google Analytics | Daily | 6 months |

| Operating costs | Accounting | Monthly | 24 months |

| Active staff | HR, Payroll | Monthly | 18 months |

Enriching Contextual Data

To improve prediction accuracy and better understand the factors that influence your business, it's recommended to include external variables:

- Commercial calendar: Holidays, long weekends, Black Friday, sales

- Weather data: Temperature, precipitation, seasonal indices

- Competitive activity: Launches, promotions, price changes

- Economic indicators: CPI, unemployment, consumer confidence

- Marketing events: Campaigns, advertising investment, media appearances

- Internal factors: Price changes, new products, expansions

Data Preparation and Cleaning

import pandas as pd

import numpy as np

from datetime import datetime

def prepare_time_series_data(data_file, date_column, value_column):

"""

Prepares and cleans data for time series analysis

"""

# Load data

df = pd.read_csv(data_file)

# Convert date

df[date_column] = pd.to_datetime(df[date_column])

# Sort by date

df = df.sort_values(date_column)

# Detect and handle missing values

print(f"Missing values detected: {df[value_column].isnull().sum()}")

# Strategies for missing values

if df[value_column].isnull().sum() > 0:

# Option 1: Linear interpolation

df[value_column + '_interpolated'] = df[value_column].interpolate(method='linear')

# Option 2: Moving average

df[value_column + '_moving_avg'] = df[value_column].fillna(

df[value_column].rolling(window=7, min_periods=1).mean()

)

# Option 3: Forward fill

df[value_column + '_forward_fill'] = df[value_column].fillna(method='ffill')

# Detect outliers using IQR method

Q1 = df[value_column].quantile(0.25)

Q3 = df[value_column].quantile(0.75)

IQR = Q3 - Q1

lower_bound = Q1 - 1.5 * IQR

upper_bound = Q3 + 1.5 * IQR

outliers = (df[value_column] < lower_bound) | (df[value_column] > upper_bound)

print(f"Outliers detected: {outliers.sum()} ({outliers.mean()*100:.1f}% of total)")

# Mark outliers but don't remove (they might be important events)

df['is_outlier'] = outliers

# Create temporal features

df['year'] = df[date_column].dt.year

df['month'] = df[date_column].dt.month

df['day'] = df[date_column].dt.day

df['day_of_week'] = df[date_column].dt.dayofweek

df['week_of_year'] = df[date_column].dt.isocalendar().week

df['quarter'] = df[date_column].dt.quarter

# Identify special days

df['is_weekend'] = df['day_of_week'].isin([5, 6])

df['is_month_start'] = df['day'] <= 5

df['is_month_end'] = df['day'] >= 26

# Calculate lag features (previous values)

for lag in [1, 7, 30, 365]:

if len(df) > lag:

df[f'lag_{lag}'] = df[value_column].shift(lag)

# Calculate moving averages

for window in [7, 30, 90]:

if len(df) >= window:

df[f'moving_avg_{window}'] = df[value_column].rolling(window=window).mean()

# Calculate growth rates

df['daily_growth'] = df[value_column].pct_change()

df['weekly_growth'] = df[value_column].pct_change(periods=7)

df['monthly_growth'] = df[value_column].pct_change(periods=30)

# Summary statistics

summary = {

'total_period': f"{df[date_column].min().date()} to {df[date_column].max().date()}",

'number_observations': len(df),

'average_frequency': (df[date_column].max() - df[date_column].min()).days / len(df),

'average_value': df[value_column].mean(),

'median_value': df[value_column].median(),

'standard_deviation': df[value_column].std(),

'coefficient_variation': df[value_column].std() / df[value_column].mean(),

'annual_growth_rate': ((df[value_column].iloc[-30:].mean() / df[value_column].iloc[:30].mean()) ** (365/((df[date_column].max() - df[date_column].min()).days)) - 1) * 100

}

print("\n=== DATA SUMMARY ===")

for key, value in summary.items():

if isinstance(value, float):

print(f"{key}: {value:.2f}")

else:

print(f"{key}: {value}")

return df, summary

def validate_data_quality(df, date_column, value_column):

"""

Validates data quality for time series analysis

"""

problems = []

# Check temporal regularity

differences = df[date_column].diff().dropna()

mode_frequency = differences.mode()[0] if len(differences.mode()) > 0 else None

irregularities = (differences != mode_frequency).sum()

if irregularities > len(df) * 0.1: # More than 10% irregular

problems.append(f"Irregular data: {irregularities} observations don't follow expected frequency")

# Check duplicates

duplicates = df[date_column].duplicated().sum()

if duplicates > 0:

problems.append(f"Duplicate dates: {duplicates} records")

# Check minimum length

if len(df) < 24: # Minimum 2 years of monthly data

problems.append(f"Insufficient data: {len(df)} observations (recommended: >24)")

# Check negative values in series that should be positive

if (df[value_column] < 0).any():

negative_values = (df[value_column] < 0).sum()

problems.append(f"Negative values detected: {negative_values} observations")

# Check variance

if df[value_column].std() == 0:

problems.append("Series without variance - all values are equal")

return problems

# Example usage

if __name__ == "__main__":

# Simulate example data

dates = pd.date_range('2022-01-01', '2024-12-31', freq='D')

values = 1000 + np.cumsum(np.random.normal(0, 10, len(dates)))

# Introduce some missing values and outliers

values[50:55] = np.nan # Missing values

values[200] = values[200] * 5 # Outlier

example_data = pd.DataFrame({

'date': dates,

'sales': values

})

# Save example

example_data.to_csv('example_data.csv', index=False)

# Prepare data

prepared_df, summary = prepare_time_series_data(

'example_data.csv', 'date', 'sales'

)

# Validate quality

problems = validate_data_quality(prepared_df, 'date', 'sales')

if problems:

print("\n⚠️ QUALITY PROBLEMS DETECTED:")

for problem in problems:

print(f"- {problem}")

else:

print("\n✅ Data suitable for time series analysis")Tangible Benefits for Planning

Implementation of AI sales forecasting through time series generates measurable benefits that directly impact the operational efficiency and profitability of the SME.

Improvement in Prediction Accuracy

| Prediction Area | Traditional Method | With Time Series | Improvement |

|---|---|---|---|

| Monthly sales | ±25% error | ±8-12% error | 52-68% better |

| Seasonal demand | ±40% error | ±10-15% error | 62-75% better |

| Cash flow | ±30% error | ±12-18% error | 40-60% better |

| Staff needs | Intuition | Quantified prediction | New capability |

| Investment timing | Reactive | Predictive | 2-6 months anticipation |

Resource Optimization

- 20-30% reduction in inventory costs through better planning

- Optimization of seasonal hiring with 2-3 months anticipation

- 15-25% improvement in installed capacity utilization

- 40-60% reduction in time dedicated to manual planning

- 25-35% decrease in immobilized working capital

Competitive Advantages

- Faster response to market changes through early trend detection

- Better customer service through optimized product/service availability

- More effective supplier negotiation based on predicted demand

- More precise financial planning for growth and expansion

- Risk reduction through better scenario anticipation

Study by the Madrid Institute of Business Studies (2024) shows that SMEs implementing time series analysis improve their operational profitability by an average of 18% during the first year.

Accessible Tools and Technologies

Time series analysis no longer requires specialized teams or expensive software. Multiple options exist that adapt to different technical levels and SME budgets.

No-Code Solutions

| Tool | Type | Monthly Price | Specialty |

|---|---|---|---|

| Excel + Power BI | Microsoft | €20-45 | Basic analysis, visualization |

| Google Sheets + Data Studio | Free-€15 | Collaboration, web reports | |

| Tableau | Specialized | €75-150 | Advanced visualization |

| Qlik Sense | BI Platform | €50-100 | Business Intelligence |

| Looker Studio | Free | Automatic dashboards | |

| Zoho Analytics | Zoho Suite | €25-50 | CRM/ERP integration |

Specialized Platforms

- Prophet (Facebook): Open source, excellent for seasonality

- Azure Machine Learning: Microsoft cloud platform

- AWS Forecast: Amazon service for time series

- Google Cloud AI Platform: ML tools in the cloud

- DataRobot: AutoML specialized in temporal prediction

- H2O.ai: Open source platform with web interface

Excel Implementation: First Step

For SMEs that prefer to start with familiar tools, Excel offers surprisingly powerful capabilities for basic time series analysis:

' VBA code to automate basic analysis in Excel

Sub AnalyzeTimeSeries()

' Set variables

Dim ws As Worksheet

Dim dateRange As Range

Dim valueRange As Range

Dim lastRow As Long

Set ws = ActiveSheet

lastRow = ws.Cells(ws.Rows.Count, "A").End(xlUp).Row

' Define data ranges

Set dateRange = ws.Range("A2:A" & lastRow)

Set valueRange = ws.Range("B2:B" & lastRow)

' Calculate trend (linear regression)

ws.Range("D1").Value = "Trend"

For i = 2 To lastRow

ws.Cells(i, 4).Formula = "=TREND($B$2:$B$" & lastRow & ",$A$2:$A$" & lastRow & ",A" & i & ")"

Next i

' Calculate moving average (12 periods)

ws.Range("E1").Value = "Moving Average 12"

For i = 13 To lastRow ' Start from period 13

ws.Cells(i, 5).Formula = "=AVERAGE(B" & (i - 11) & ":B" & i & ")"

Next i

' Calculate growth from previous period

ws.Range("F1").Value = "Growth %"

For i = 3 To lastRow

ws.Cells(i, 6).Formula = "=(B" & i & "-B" & (i - 1) & ")/B" & (i - 1)

ws.Cells(i, 6).NumberFormat = "0.0%"

Next i

' Identify seasonality (comparison with previous year)

ws.Range("G1").Value = "Seasonal"

For i = 14 To lastRow ' Start from month 14 to have complete year

ws.Cells(i, 7).Formula = "=B" & i & "/B" & (i - 12)

Next i

' Create automatic chart

Dim chart As ChartObject

Set chart = ws.ChartObjects.Add(Left:=350, Top:=50, Width:=400, Height:=250)

With chart.Chart

.ChartType = xlLineMarkers

.SetSourceData Source:=Union(dateRange, valueRange)

.HasTitle = True

.ChartTitle.Text = "Time Series Analysis"

.Axes(xlCategory).HasTitle = True

.Axes(xlCategory).AxisTitle.Text = "Date"

.Axes(xlValue).HasTitle = True

.Axes(xlValue).AxisTitle.Text = "Value"

End With

' Calculate descriptive statistics

ws.Range("I1").Value = "Statistics"

ws.Range("I2").Value = "Average:"

ws.Range("J2").Formula = "=AVERAGE(B:B)"

ws.Range("I3").Value = "Median:"

ws.Range("J3").Formula = "=MEDIAN(B:B)"

ws.Range("I4").Value = "Std Deviation:"

ws.Range("J4").Formula = "=STDEV(B:B)"

ws.Range("I5").Value = "Coef. Variation:"

ws.Range("J5").Formula = "=J4/J2"

ws.Range("J5").NumberFormat = "0.0%"

' Simple prediction (next 3 months)

ws.Range("I7").Value = "Predictions:"

For i = 1 To 3

ws.Cells(7 + i, 9).Value = "Month +" & i & ":"

ws.Cells(7 + i, 10).Formula = "=FORECAST(A" & lastRow & "+" & (i * 30) & ",B:B,A:A)"

Next i

MsgBox "Analysis completed. Review results in columns D-J."

End Sub

' Function to detect outliers

Function IsOutlier(value As Double, range As Range) As Boolean

Dim Q1 As Double, Q3 As Double, IQR As Double

Q1 = Application.WorksheetFunction.Quartile(range, 1)

Q3 = Application.WorksheetFunction.Quartile(range, 3)

IQR = Q3 - Q1

If value < (Q1 - 1.5 * IQR) Or value > (Q3 + 1.5 * IQR) Then

IsOutlier = True

Else

IsOutlier = False

End If

End Function

' Macro to identify trends

Sub IdentifyTrends()

Dim ws As Worksheet

Dim lastRow As Long

Dim slope As Double

Set ws = ActiveSheet

lastRow = ws.Cells(ws.Rows.Count, "A").End(xlUp).Row

' Calculate trend slope

slope = Application.WorksheetFunction.Slope(ws.Range("B2:B" & lastRow), ws.Range("A2:A" & lastRow))

' Interpret trend

ws.Range("I12").Value = "Trend:"

If slope > 0.1 Then

ws.Range("J12").Value = "Growing"

ElseIf slope < -0.1 Then

ws.Range("J12").Value = "Declining"

Else

ws.Range("J12").Value = "Stable"

End If

ws.Range("I13").Value = "Slope:"

ws.Range("J13").Value = Round(slope, 4)

End SubPractical Implementation Guide

Successful implementation of AI planning requires a structured approach that minimizes initial complexity while progressively building analytical capabilities.

Phase 1: Diagnosis and Preparation (Weeks 1-2)

- Identify all temporal data sources available in the company

- Evaluate the quality, frequency, and completeness of each source

- Select 2-3 critical series for the business (sales, customers, inventory)

- Establish specific objectives: what do we want to predict and with what accuracy?

- Assign internal project manager and define initial budget

Phase 2: Exploratory Analysis (Weeks 3-4)

- Clean and normalize selected historical data

- Perform basic decomposition: trend, seasonality, noise

- Identify patterns, cycles, and significant anomalous events

- Document findings and generate hypotheses about causal factors

- Create first visual dashboards for continuous monitoring

Phase 3: Modeling and Prediction (Weeks 5-8)

- Implement basic models (moving averages, linear regression)

- Develop advanced models (Holt-Winters, ARIMA) according to needs

- Validate accuracy using historical data (backtesting)

- Adjust parameters to optimize accuracy/simplicity balance

- Create alert system for significant deviations

Phase 4: Operational Integration (Weeks 9-12)

- Integrate predictions into existing planning processes

- Train team in interpretation and use of predictions

- Establish model update and monitoring routines

- Implement feedback loops for continuous improvement

- Document processes and create internal user manual

Success Metrics and Monitoring

Defining clear metrics from the start allows objective evaluation of the impact of time series analysis and justifies future investments in analytical capabilities.

Model Accuracy KPIs

| Metric | Description | Target | Measurement Frequency |

|---|---|---|---|

| MAPE | Mean absolute percentage error | <15% | Monthly |

| MAE | Mean absolute error | Variable by context | Monthly |

| Directional accuracy | % correct direction change | >70% | Quarterly |

| R² | Coefficient of determination | >0.7 | Quarterly |

| Stability | Month-to-month consistency | ±5% variation | Monthly |

Business Impact KPIs

| Area | Metric | Baseline | 6m Target | 12m Target |

|---|---|---|---|---|

| Planning | Planning time | 20h/month | 12h/month | 8h/month |

| Inventory | Stock turnover | 4x/year | 5x/year | 6x/year |

| Staff | Hiring accuracy | 60% | 80% | 90% |

| Finance | Cash flow accuracy | ±30% | ±15% | ±10% |

| Operations | Capacity utilization | 65% | 75% | 85% |

import pandas as pd

import numpy as np

from datetime import datetime, timedelta

import matplotlib.pyplot as plt

class TimeSeriesMonitor:

def __init__(self):

self.metrics_history = []

self.thresholds = {

'max_mape': 15,

'min_directional_accuracy': 70,

'min_r2': 0.7

}

def evaluate_model(self, dates, actual_values, predictions, series_name="Series"):

"""

Evaluates model performance and updates historical metrics

"""

# Calculate basic metrics

mape = np.mean(np.abs((actual_values - predictions) / actual_values)) * 100

mae = np.mean(np.abs(actual_values - predictions))

rmse = np.sqrt(np.mean((actual_values - predictions)**2))

# R² (coefficient of determination)

ss_res = np.sum((actual_values - predictions)**2)

ss_tot = np.sum((actual_values - np.mean(actual_values))**2)

r2 = 1 - (ss_res / ss_tot) if ss_tot != 0 else 0

# Directional accuracy (correctly predict ups/downs)

actual_changes = np.diff(actual_values) > 0

predicted_changes = np.diff(predictions) > 0

directional_accuracy = np.mean(actual_changes == predicted_changes) * 100

# Model bias

bias = np.mean((predictions - actual_values) / actual_values) * 100

# Create evaluation record

evaluation = {

'evaluation_date': datetime.now(),

'series': series_name,

'period_evaluated': f"{dates[0]} to {dates[-1]}",

'num_observations': len(actual_values),

'mape': mape,

'mae': mae,

'rmse': rmse,

'r2': r2,

'directional_accuracy': directional_accuracy,

'bias': bias,

'meets_mape': mape <= self.thresholds['max_mape'],

'meets_accuracy': directional_accuracy >= self.thresholds['min_directional_accuracy'],

'meets_r2': r2 >= self.thresholds['min_r2']

}

self.metrics_history.append(evaluation)

return evaluation

def generate_quality_alert(self, evaluation):

"""

Generates alerts based on model quality

"""

alerts = []

if not evaluation['meets_mape']:

alerts.append(f"⚠️ High MAPE: {evaluation['mape']:.1f}% (target: <{self.thresholds['max_mape']}%)")

if not evaluation['meets_accuracy']:

alerts.append(f"⚠️ Low directional accuracy: {evaluation['directional_accuracy']:.1f}% (target: >{self.thresholds['min_directional_accuracy']}%)")

if not evaluation['meets_r2']:

alerts.append(f"⚠️ Low R²: {evaluation['r2']:.3f} (target: >{self.thresholds['min_r2']})")

if abs(evaluation['bias']) > 10:

alerts.append(f"⚠️ Significant bias: {evaluation['bias']:.1f}% (model consistently over/underestimates)")

return alerts

def performance_dashboard(self):

"""

Creates model performance dashboard

"""

if len(self.metrics_history) == 0:

print("No historical data to display")

return

df = pd.DataFrame(self.metrics_history)

fig, axes = plt.subplots(2, 2, figsize=(15, 10))

# MAPE evolution

axes[0,0].plot(df['evaluation_date'], df['mape'], marker='o')

axes[0,0].axhline(y=self.thresholds['max_mape'], color='r', linestyle='--', label=f'Target (<{self.thresholds["max_mape"]}%)')

axes[0,0].set_title('MAPE Evolution')

axes[0,0].set_ylabel('MAPE (%)')

axes[0,0].legend()

axes[0,0].grid(True, alpha=0.3)

# Directional accuracy

axes[0,1].plot(df['evaluation_date'], df['directional_accuracy'], marker='s', color='green')

axes[0,1].axhline(y=self.thresholds['min_directional_accuracy'], color='r', linestyle='--', label=f'Target (>{self.thresholds["min_directional_accuracy"]}%)')

axes[0,1].set_title('Directional Accuracy')

axes[0,1].set_ylabel('Accuracy (%)')

axes[0,1].legend()

axes[0,1].grid(True, alpha=0.3)

# R²

axes[1,0].plot(df['evaluation_date'], df['r2'], marker='^', color='orange')

axes[1,0].axhline(y=self.thresholds['min_r2'], color='r', linestyle='--', label=f'Target (>{self.thresholds["min_r2"]})')

axes[1,0].set_title('Coefficient of Determination (R²)')

axes[1,0].set_ylabel('R²')

axes[1,0].legend()

axes[1,0].grid(True, alpha=0.3)

# Error distribution

axes[1,1].hist(df['mape'], bins=10, alpha=0.7, color='skyblue', edgecolor='black')

axes[1,1].axvline(x=self.thresholds['max_mape'], color='r', linestyle='--', label=f'Target (<{self.thresholds["max_mape"]}%)')

axes[1,1].set_title('Error Distribution (MAPE)')

axes[1,1].set_xlabel('MAPE (%)')

axes[1,1].set_ylabel('Frequency')

axes[1,1].legend()

axes[1,1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

return fig

def summary_report(self):

"""

Generates executive performance report

"""

if len(self.metrics_history) == 0:

return "No data to generate report"

df = pd.DataFrame(self.metrics_history)

# General statistics

report = {

'analysis_period': f"{df['evaluation_date'].min().date()} to {df['evaluation_date'].max().date()}",

'number_evaluations': len(df),

'average_mape': df['mape'].mean(),

'best_mape': df['mape'].min(),

'worst_mape': df['mape'].max(),

'average_directional_accuracy': df['directional_accuracy'].mean(),

'average_r2': df['r2'].mean(),

'mape_compliance_percentage': (df['meets_mape'].sum() / len(df)) * 100,

'accuracy_compliance_percentage': (df['meets_accuracy'].sum() / len(df)) * 100,

'r2_compliance_percentage': (df['meets_r2'].sum() / len(df)) * 100,

'improvement_trend': df['mape'].iloc[-3:].mean() < df['mape'].iloc[:3].mean() if len(df) >= 6 else None

}

# Generate recommendations

recommendations = []

if report['average_mape'] > self.thresholds['max_mape']:

recommendations.append("Review model: average MAPE above target")

if report['mape_compliance_percentage'] < 70:

recommendations.append("Consider retraining: low MAPE target compliance")

if report['average_r2'] < 0.6:

recommendations.append("Evaluate additional variables: low model explanatory power")

if report['improvement_trend'] is False:

recommendations.append("Investigate degradation: model is getting worse over time")

report['recommendations'] = recommendations

return report

# Example usage

monitor = TimeSeriesMonitor()

# Simulate monthly evaluations

for i in range(6):

# Generate simulated data

dates = pd.date_range(start=datetime.now() - timedelta(days=30*(i+1)), periods=30, freq='D')

actual_values = np.random.normal(1000, 100, 30)

# Simulate predictions with some error

predictions = actual_values + np.random.normal(0, 50, 30)

evaluation = monitor.evaluate_model(dates, actual_values, predictions, "Sales")

alerts = monitor.generate_quality_alert(evaluation)

if alerts:

print(f"\nMonth {i+1} - Alerts detected:")

for alert in alerts:

print(alert)

# Generate final report

report = monitor.summary_report()

print("\n=== EXECUTIVE PERFORMANCE REPORT ===")

print(f"Analysis period: {report['analysis_period']}")

print(f"Average MAPE: {report['average_mape']:.1f}%")

print(f"MAPE target compliance: {report['mape_compliance_percentage']:.0f}%")

print(f"Directional accuracy: {report['average_directional_accuracy']:.1f}%")

if report['recommendations']:

print("\nRecommendations:")

for rec in report['recommendations']:

print(f"- {rec}")Common Mistakes and How to Avoid Them

Implementation of time series analysis presents specific challenges that can compromise results if not properly addressed from the project's inception.

Mistake 1: Insufficient or Irregular Data

Problem: Attempting analysis with less than 2 complete data cycles. Solution: Collect minimum 24 months for annual seasonality, 14 days for weekly patterns.

Mistake 2: Ignoring Stationarity

- Problem: Applying models that assume stationary data to series with clear trend

- Symptoms: Predictions that consistently deviate, models that 'explode'

- Solution: Series differencing, logarithmic transformations, detrending

- Tool: Dickey-Fuller test to verify stationarity

Mistake 3: Overfitting on Small Data

SMEs with little historical data tend to create models that memorize rather than generalize. Use temporal cross-validation and prefer simple models with few variables until you have more data.

Mistake 4: Not Considering Exceptional Events

- Include dummy variables for promotions, launches, crises

- Document unique events that won't repeat

- Adjust historical data for known non-recurring events

- Create alternative scenarios for similar future events

System Scaling and Evolution

A successful time series implementation must evolve with SME growth, gradually adding capabilities and sophistication according to available needs and resources.

Evolution Roadmap

| Stage | Duration | Capabilities | Estimated Investment |

|---|---|---|---|

| Basic | 3-6 months | Excel, charts, simple trends | €500-2,000 |

| Intermediate | 6-12 months | BI software, automated models | €2,000-8,000 |

| Advanced | 12-18 months | Automatic ML, multiple series | €5,000-15,000 |

| Expert | 18+ months | Predictive AI, real-time | €10,000-25,000 |

Integration with Other Systems

- ERP: Automatic integration of financial and operational data

- CRM: Customer behavior analysis and lifecycle

- E-commerce: Traffic, conversion and abandonment prediction

- HR: Workforce planning based on demand cycles

- Logistics: Inventory and supply chain optimization

Conclusion: Transform Data into Strategic Decisions

Time series analysis represents one of the most profitable investments an SME can make in analytical capabilities. Unlike other technologies that require complex infrastructures, time series work with data you already possess and tools you can implement gradually.

The benefits transcend simple number prediction: it's about transforming intuition into information, reactivity into proactivity, and uncertainty into strategic confidence. SMEs that master these analyses make more informed decisions, plan with greater precision, and navigate market uncertainty with significant competitive advantages.

The question is not whether your SME needs time series analysis, but when you will begin leveraging the hidden patterns in your historical data. Every day that passes without analysis is a lost opportunity for optimization and improvement.

Start today: take your sales data from the last 12 months, create them in Excel and calculate the 3-month moving average. That smoothed line is your first trend prediction. In 30 days, you can have a complete system running. Your strategic planning will never be the same again.